Skip to main content

Company Payroll

Show submenu for About

About

About Us

Reviews

Timesheet Submission

Show submenu for Payroll Support

Payroll Support

Becoming an Employer

Payroll Deadlines

FAQ'S

Employing a PA

Insurance for Employing a PA

Your PA's Holiday Entitlement

Show submenu for PAYE payments to HMRC

PAYE payments to HMRC

Paying HMRC via Brightpay Connect

Keeping your information up to date

Useful Links

Show submenu for Forms

Forms

Submit a Timesheet

Tell us about a change

Access your Payroll online

News

Open main navigation

Close main navigation

Company Payroll

Show submenu for About

About

About

About

About Us

Reviews

Timesheet Submission

Show submenu for Payroll Support

Payroll Support

Payroll Support

Payroll Support

Becoming an Employer

Payroll Deadlines

FAQ'S

Employing a PA

Insurance for Employing a PA

Your PA's Holiday Entitlement

Show submenu for PAYE payments to HMRC

PAYE payments to HMRC

PAYE payments to HMRC

PAYE payments to HMRC

Paying HMRC via Brightpay Connect

Keeping your information up to date

Useful Links

Show submenu for Forms

Forms

Forms

Forms

Submit a Timesheet

Tell us about a change

Access your Payroll online

News

Contact

Call 0800 029 7070

March 2026 Payroll Deadlines

Posted by

admin

,

Mar 5, 2026 12:33:57 PM

Read More

Mar 5, 2026 12:30:57 PM

•

1 min read

Employees P60s to Arrive with March Payroll

Mar 5, 2026 12:25:53 PM

•

2 min read

Understanding Your Employee’s Holiday Accrual

Feb 6, 2026 1:25:07 PM

•

1 min read

Show your employee some love this Valentine month – tips on being a ‘good’ employer

Feb 6, 2026 1:19:45 PM

•

3 min read

Being a Successful Employer When You Employ Your Own Carer (UK)

Jan 22, 2026 9:40:56 AM

•

0 min read

February 2026 Payroll Deadlines

Jan 8, 2026 10:50:45 AM

•

2 min read

Checking your PA’s holiday

Jan 8, 2026 10:46:31 AM

•

0 min read

National Living Wage Increase for 2026/27

Jan 8, 2026 10:41:57 AM

•

3 min read

Making your PAYE payments

Dec 17, 2025 11:17:04 AM

•

0 min read

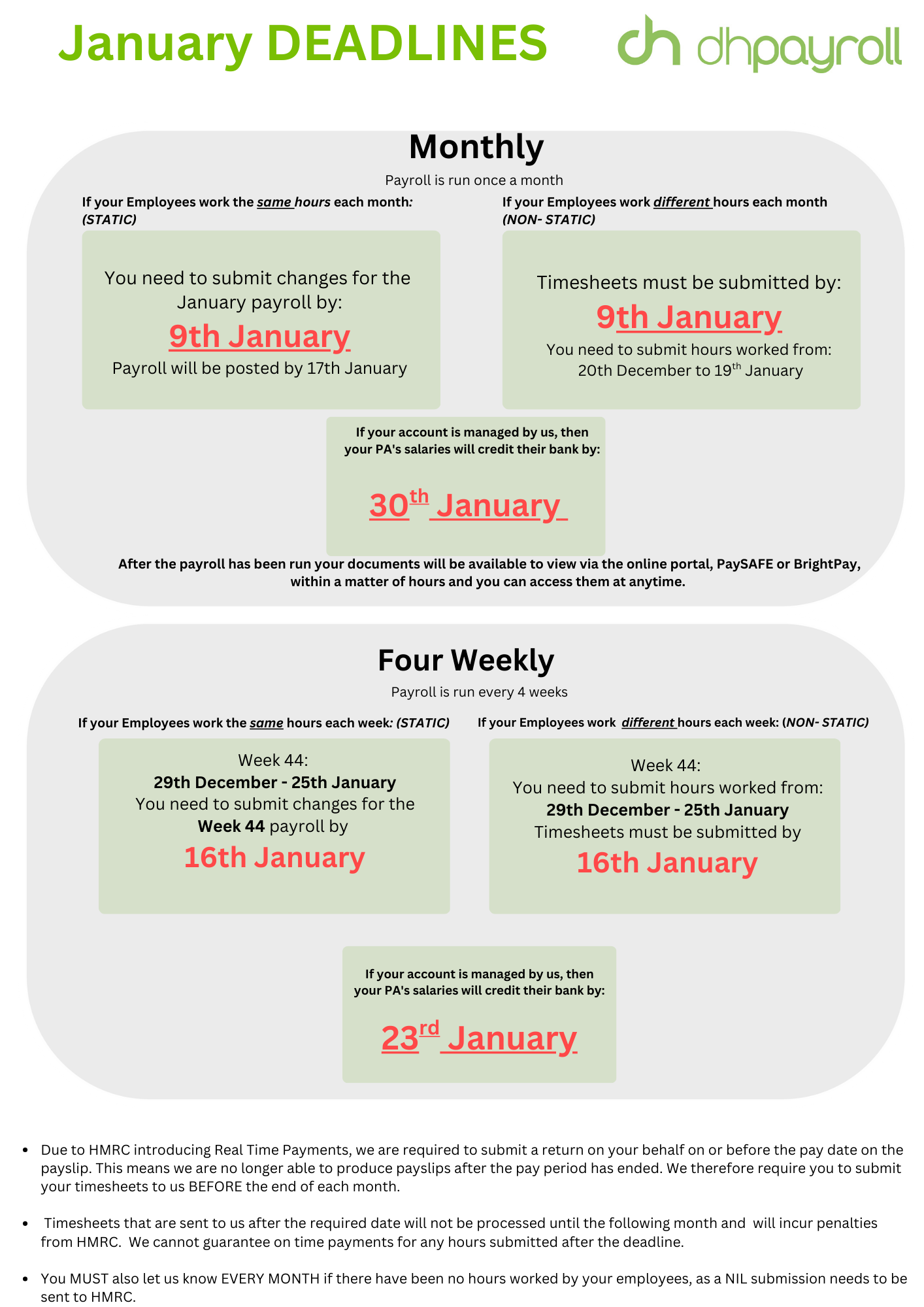

January 2026 Payroll Deadline

1

2

3

4

5

All

Next

%20(1).jpg)

.jpg)

%20(1)%20(1).jpg)

.jpg)

-3.png)

.jpg)

%20(1).webp)